Overview

This section provides information on the following topics to assist in preparing cost data for submission to CMS' RDS Center:

- Who Should Submit Drug Cost Data

- What Has to Happen Before Cost Data May Be Submitted

- Frequency for Reporting Cost Data to CMS' RDS Center

- Key Terms for Preparing Costs

- What Cost Data to Submit

- Reporting Estimated Percentage of Premiums Instead of Gross Retiree Costs: Option for Fully-Insured Plans

- Reporting Cost Adjustments

- Reporting Revised Cost Data

- Working With a Vendor to Aggregate and Send Cost Data to CMS' RDS Center

- Aggregating Cost Data if Multiple Vendors are Reporting Cost Data for a Single Benefit Option

Who Should Submit Drug Cost Data

Plan Sponsors and Vendors must submit cost data to CMS' RDS Center before submitting an interim or Reconciliation payment request.

Before submitting cost data, cost preparers compile incurred costs of Medicare Part D drugs by Benefit Option and Plan Month for Qualifying Covered Retirees (QCRs) that are eligible for subsidy under the RDS Program. The function of the cost preparer happens outside of the RDS system and may or may not be the same individual(s) assigned the Report Costs privilege in the RDS Secure Website. Regardless, communicating with these individuals is important. It is recommended that the Account Manager coordinate communication among all individuals involved.

Once costs are prepared, cost reporters report cost data to CMS' RDS Center for QCRs by Manual Data Entry on the RDS Secure Website or by Connect:Direct. A Cost Reporter may be the Account Manager, Plan Sponsor Designee, Vendor, or Vendor Designee.

What Has to Happen Before Cost Data May Be Submitted

Before cost data may be submitted using the RDS Secure Website, the application must be submitted and approved, and Payment Setup must be completed. For more information, refer to Payment Setup.

Before preparing cost data, retiree changes should be submitted to CMS' RDS Center in a Retiree List. The resulting Retiree Response File must then be processed. It is good practice to request the Covered Retiree List (CRL) and distribute it to cost preparers for review; costs may only be reported for the QCRs, Benefit Options, and Subsidy Periods listed in the CRL.

At Reconciliation, cost data may only be submitted after the CRL is finalized in Reconciliation: Finalize Covered Retirees. Until this step is complete, events may occur that change the CRL, such as a notification from the Medicare Beneficiary Database (MBD) or submission of a new retiree file. Should these events occur, the RDS Secure Website will force you to request and download a new CRL. Once Reconciliation: Finalize Covered Retirees is complete, new retiree files will be rejected and notifications will be held.

Frequency for Reporting Cost Data to CMS' RDS Center

The frequency with which cost data are reported to CMS' RDS Center is at the discretion of the Plan Sponsor. There is no limit to the number of times cost data can be submitted or resubmitted for a given month. Reported cost data submitted to CMS' RDS Center are used to build payment requests; therefore, cost data must be submitted before a payment request can be created and submitted by the Plan Sponsor. Payments can only be requested for the month(s) in which cost data has been reported. Additionally, the Interim Monthly Payment Frequency allows Plan Sponsors to make a maximum of 12 interim payment requests for a plan year. Although 12 interim payment requests are permitted, a Plan Sponsor may choose to submit fewer than 12 interim payment requests.

Key Terms for Preparing Costs

Cost reporters should familiarize themselves with all of the following terms:

- Gross Retiree Costs: Non-administrative costs incurred under the plan for Medicare Part D drugs (as defined in 42 C.F.R. §423.100), whether paid by the Plan Sponsor or retiree, or a combination. Gross Retiree Costs must be reported for all months in the plan year. Premium costs are not considered Gross Retiree Costs for purposes of final cost reports and cannot be reported in place of or in addition to Gross Retiree Costs.

- Estimated Premiums: Estimated percentage of premiums is the portion of premium costs (excluding administrative costs, risk charges, etc.) paid by the Plan Sponsor and by the Qualifying Covered Retiree that, based on a determination by the insurer using reasonable actuarial principles, is allocated to Gross Retiree Costs between the Cost Threshold and the Cost Limit. Estimated premiums cannot be submitted as final costs during Reconciliation. Actual gross costs must be reported during Reconciliation.

- Cost Threshold: The Federally-defined amount of out-of-pocket expenses paid by, or on behalf of, the beneficiary. The amount up to the Cost Threshold is not eligible for subsidy. It is adjusted in the same manner as the annual Medicare Part D deductible and the annual Medicare Part D out of pocket threshold and is adjusted annually as defined in 42 C.F.R. §423.104(d)(1)(ii) and (d)(5)(iii)(B), respectively. The Cost Threshold is calculated based on Plan Year End Date. For more information on Cost Threshold amounts, refer to Cost Threshold and Cost Limit by Plan Year.

- Cost Limit: The Federally-defined amount of out-of-pocket expenses paid by, or on behalf of, the beneficiary. The amount exceeding the Cost Limit is not eligible for subsidy. It is adjusted in the same manner as the annual Medicare Part D deductible and the annual Medicare Part D out of pocket limit and is adjusted annually as defined in 42 C.F.R. §423.104(d)(1)(ii) and (d)(5)(iii)(B), respectively. The Cost Limit is calculated based on Plan Year End Date. For more information on Cost Limit amounts, refer to Cost Threshold and Cost Limit by Plan Year.

- Threshold Reduction: Gross Retiree Costs below the Federally defined Cost Threshold are not eligible for the subsidy. This amount is referred to as the Threshold Reduction. Gross Retiree Costs will be reduced by the Threshold Reduction when calculating subsidy. The Threshold Reduction amount must be calculated per Qualifying Covered Retiree and aggregated by Benefit Option and plan month. For more information on accurately calculating Threshold Reduction, refer to Underreporting Threshold Reduction and Limit Reduction. Note: The Threshold Reduction is required for at least the first month in the plan year where gross costs were reported. For subsequent months, the Threshold Reduction is not required; however, it must be provided as applicable.

- Limit Reduction: The amount of Gross Retiree Costs in excess of the Federally defined Cost Limit is not eligible for the subsidy. This ineligible excess amount is referred to as the Limit Reduction. Gross Retiree Costs will be reduced by the Limit Reduction when calculating subsidy. The Limit Reduction amount must be calculated per Qualifying Covered Retiree and aggregated by Benefit Option and plan month. For more information on accurately calculating Limit Reduction, refer to Underreporting Threshold Reduction and Limit Reduction.

- Cost Adjustments: Any discounts, chargebacks, rebates, and/or other price concessions given by the manufacturer or pharmacy to the Plan Sponsor that are attributable to Gross Retiree Costs between the Cost Threshold and Cost Limit. The Cost Adjustment must be reported to CMS' RDS Center, as those amounts need to be accounted for, to determine the Allowable Retiree Cost. Estimated Cost Adjustments are only used in interim cost reporting. At Reconciliation, the Actual Cost Adjustment must be reported. For more information on reporting Estimated versus Actual Cost Adjustments, refer to Reporting Cost Adjustments.

What Cost Data to Submit

Cost Reporting Data Elements

When reporting Gross Retiree Cost data for self-funded Benefit Options or fully-insured Benefit Options, the Plan Sponsor must submit aggregated cost data for all retirees covered under the Benefit Option in the following data elements:

- For Interim Cost Reporting: Gross Retiree Costs, Threshold Reduction, Limit Reduction, and Estimated Cost Adjustment.

- For Reconciliation (Final) Cost Reporting: Gross Retiree Costs, Threshold Reduction, Limit Reduction, and Actual Cost Adjustment.

When reporting Estimated Premiums for fully-insured Benefit Options, the only data element required by CMS' RDS Center is the Estimated Premium, which needs to be aggregated for all retirees for the reported month. However, if the Estimated Premium cost amount does not include the Estimated Cost Adjustment, that sum must be reported as a separate data element.

Determining What Gross Retiree Cost Data to Include in a Cost Report

Cost data may only be submitted for the QCRs, Benefit Options, and subsidy periods listed on the CRL. Therefore, it is imperative to submit monthly Retiree Lists containing appropriate add/update/delete records to CMS' RDS Center to ensure the CRL provided for an application is as current as possible. The Account Manager should then distribute the CRL to cost preparers.

Before submitting cost data, review the current subsidy periods on the CRL for the application, and submit only Gross Retiree Costs incurred during the month being reported, within the subsidy period for a given retiree. Additionally, if reporting estimated percentage of premiums, include only retirees with valid subsidy periods for the month in which cost data is being submitted.

Cost reports submitted to CMS' RDS Center for a Benefit Option are aggregated for all retirees by month—based on the month the drug costs were incurred (i.e., prescription filled and purchased by retiree or on their behalf).

Example: 100 retirees are covered under the Benefit Option and the Plan Sponsor wishes to report costs for the month of January. To calculate the total for January, add up all the eligible gross retiree cost data for those retirees incurred in January and subsequently paid (in January or at a later date) and then submit that information to CMS' RDS Center. Repeat the process for each month in the plan year in which eligible costs were incurred.

Determining Eligible Costs

There are three main criteria to determine if drug costs for a retiree are eligible for subsidy:

- Drug is covered under Medicare Part D - Gross drug costs must be covered under Medicare Part D as defined in 42 C.F.R. 423.100. Gross costs include dispensing fees, ingredient costs, and sales tax, but exclude administrative costs. For more guidance on what constitutes a Part D drug, refer to Chapter 6 of the Medicare Part D Manual, specifically Appendix C – Medicare Part B versus Part D Coverage Issues, and How to Extract Certain Medicare Part B Costs from RDS Payment Requests.

- Drug costs that are incurred (i.e., prescription filled and purchased by retiree or on their behalf) on, or within a retiree's Subsidy Period Effective Date and the Subsidy Period Termination Date – When trying to determine if a retiree's drug cost is eligible for the subsidy, the only date that is relevant is the prescription incurred (i.e., filled) date--not the paid date. If the incurred date falls within, or on the retiree's subsidy effective and termination dates, the drug cost is eligible for the subsidy if it also meets the other two criteria.

- Drug costs that are paid – The retiree's prescription must be paid to be considered an eligible drug cost for the subsidy. The drug cost can either be paid by the plan, by the retiree due to an out-of-pocket copay or deductible, or a combination. Regardless of the date the drug is paid—for example, if it was paid the day it was incurred (prescription filled) or six months later—it is still eligible, as long as it is paid and meets the other two criteria.

Maintaining Claim-Specific Data

Plan Sponsors are not required to submit claim-specific data to CMS' RDS Center for cost reporting. However, claims data must be maintained by the Plan Sponsor for a minimum of six years (which can be extended by CMS in certain circumstances) for audit purposes.

Federal regulations require that Plan Sponsors participating in the RDS Program make a final Reconciliation submission using final cost data for the plan year and data on actual rebates and other price concessions.

For example, aggregated data for Reconciliation will be reported by Benefit Option and month incurred, using the same submission methods (Data Entry or Connect:Direct file transfer) and file layouts as interim payment cost reporting. Aggregate data is not required to be reported at the individual retiree level. However, Plan Sponsors and other entities assisting them in the cost reporting process are reminded that Allowable Retiree Costs are determined at the retiree level, and records need to be retained showing how data submitted in the cost reporting process is determined. For more information on compliance and record retention, refer to the RDS Plan Sponsor Agreement.

The cost data submitted by the Plan Sponsor to CMS' RDS Center will be aggregated per retiree at the Benefit Option level within an application by month. For example:

Plan Sponsor ID

- Application ID

- Benefit Option

- January – report cost data

- February – report cost data

- March – report cost data

- April – report cost data

- Benefit Option

CRLs should be validated by the persons responsible for coordinating retiree eligibility for the Benefit Options within an application. The Plan Sponsor must work with all Cost Reporters to ensure that the cost data being reported are only for the beneficiaries and subsidy periods listed in this file. Be sure that Cost Reporters are aware of the need to coordinate thresholds and limits within an application for each beneficiary. For more information, refer to Coordination of Individual Retiree Cost Data.

Reporting Estimated Percentage of Premiums Instead of Gross Retiree Costs: Option for Fully-Insured Plans

Self-funded plans must report Gross Retiree Costs. However, plans that are fully insured have the option to report Gross Retiree Costs or Estimated Percentage of Premiums. The estimated premium option is recommended for those fully-insured plans that do not have access to retirees' gross drug costs. Estimated Percentage of Premiums is the portion of premium costs (excluding administrative costs, risk charges, etc.) paid by the Plan Sponsor and by the Qualifying Covered Retiree that, based on a determination by the insurer using reasonable actuarial principles, is allocated to Gross Retiree Costs between the Cost Threshold and the Cost Limit. If the Benefit Option includes more than one drug plan, and one of those plans is fully-insured, but the other is self-insured, gross costs must be reported and reporting Estimated Percentage of Premiums is not an option.

If the estimated premium cost amount does not include the Estimated Cost Adjustment, then that sum must be reported separately in the Estimated Cost Adjustment column.

Reporting Cost Adjustments

Cost Adjustments are any discounts, chargebacks, rebates, and/or other price concessions given by the manufacturer or pharmacy to the Plan Sponsor that are attributable to Gross Retiree Costs between the Cost Threshold and Cost Limit. Cost Adjustments are not eligible for subsidy. Cost Adjustments need to be reported to CMS' RDS Center, as those amounts must be accounted for, to determine the Allowable Retiree Cost.

For information on allocating rebates and other price concessions, review CMS Retiree Drug Subsidy Guidance: Rebates and Other Price Concessions.

Cost Adjustments During Interim Cost Reporting

During interim cost reporting, Plan Sponsors are required to report Estimated Cost Adjustments. The Estimated Cost Adjustment is based on historical data and generally accepted actuarial principles. Plan Sponsors only need to report Estimated Cost Adjustments for the gross cost between the Threshold Reduction and the Limit Reduction. Estimated Cost Adjustments must be allocated to each individual retiree's cost; however, Plan Sponsors are not required to allocate the rebates based on the individual retiree's actual usage of the specific Medicare Part D drugs for which the Plan Sponsor receives rebates. Plan Sponsors may instead choose to allocate rebates using a methodology that determines rebates received under the plan as a percentage of incurred drug costs (for example 4%) and apply that percentage to the Gross Retiree Costs between the Threshold Reduction and Limit Reduction.

Cost Adjustments During Reconciliation (Final) Cost Reporting

At Reconciliation, Plan Sponsors are required to report the actual amount of discounts, chargebacks, rebates, and other price concessions received, aggregated by Benefit Option and plan month. Plan Sponsors that used a methodology for estimating rebates for interim payments are encouraged to review their method each year. Reconciliation results in an overpayment for some Plan Sponsors due to underestimating the Estimated Cost Adjustment during interim payments. The final Actual Cost Adjustment must be reported in the same field as the Estimated Cost Adjustment when submitting cost reports by Connect:Direct file transfer. CMS' RDS Center distinguishes interim cost reports from final cost reports based on the status of the application.

Reporting Revised Cost Data

It is very likely that adjusted or additional drug cost data will be received for months where costs have been previously reported to CMS' RDS Center. For example, in July, May's drug cost data is reported; however, in August additional claims data for a drug cost incurred in May is received. When this occurs, the Plan Sponsor/cost reporter must re-aggregate the cost data for May in order to include the new information, and then resubmit the cost data for May and any subsequent months affected by the revised retiree cost data. This is necessary because Threshold Reduction and Limit Reductions for individual retirees may have affected the amounts reported in subsequent months. All cumulative cost data is required to be reported again, not just the adjustment amounts. Cost reports submitted to CMS' RDS Center can be revised as often as necessary, whenever necessary, until Reconciliation is completed.

Note: Changes to a QCR's subsidy periods could also change previously reported cost data. This is why it is very important to process the Retiree Response Files and Weekly Notification Files provided by CMS' RDS Center, and to send the monthly add/update/delete retiree files as applicable. For more information, refer to Process Retiree Response Files and Process Weekly Notification Files.

Working with a Vendor to Aggregate and Send Cost Data to CMS' RDS Center

The term "Vendor" refers to a Pharmacy Benefit Manager (PBM), Health Plan, or another third-party company that has been contracted by one or multiple Plan Sponsors to report cost data. Vendors submitting cost data on behalf of a Plan Sponsor must obtain a Vendor ID from CMS' RDS Center. To initiate the Vendor registration process, the Vendor needs to contact CMS' RDS Center. Once the Vendor receives the Vendor ID, they will need to communicate that Vendor ID number to the appropriate Plan Sponsor(s), so it can be entered in the RDS Secure Website as applicable. For more information, refer to the Vendor Quick Start Guide.

If a Vendor currently has a Vendor ID related to the RDS retiree file processing, CMS' RDS Center allows them to use their current Vendor ID to file cost reports; however, they still need to contact CMS' RDS Center for confirmation. If a Vendor plans on submitting cost data using both Connect:Direct and Data Entry (RDS Secure Website), they will need a different Vendor ID for each cost reporting method.

If a Vendor is engaged for cost data aggregation and/or submissions, the Plan Sponsor will still be able to view the data submitted by the Vendor to CMS' RDS Center, using the RDS Secure Website.

Aggregating Cost Data if Multiple Vendors are Reporting Cost Data for a Single Benefit Option

Assuming the two Vendors are managing different groups of retirees, multiple Vendors may report cost data for one Benefit Option. All Vendors reporting for the same Benefit Option must report using the same methodology (gross cost or Estimated Premiums). Plan Sponsors who have multiple Vendors reporting cost data, for the same Benefit Option or group of retirees, must coordinate individual retiree's cost data. For more information, refer to Coordination of Individual Retiree Cost Data.

Cost Reporting Examples

This section provides the following cost reporting examples:

- Cost Reporting Example Illustrating Estimated Premiums

- Cost Reporting Example Illustrating Gross Retiree Costs

- Cost Reporting Example Illustrating Threshold Reductions

- Cost Reporting Example Illustrating Limit Reductions

- Cost Reporting Example Illustrating Estimated Cost Adjustments

- Cost Reporting Example Illustrating Multiple Benefit Options Reported Over Several Months

- Cost Reporting Example Illustrating Reporting Adjusted Costs

- Cost Reporting Example Illustrating Gross Eligible Costs Exceeding Maximum Possible Gross Eligible

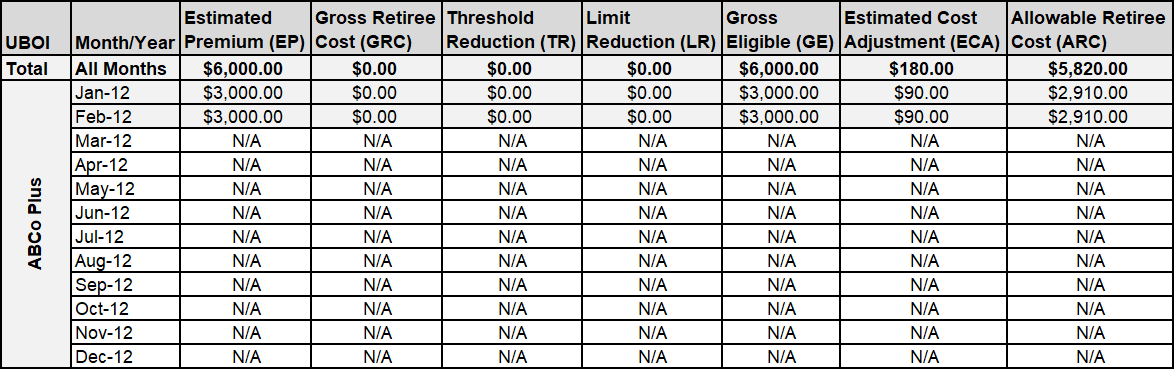

Cost Reporting Example Illustrating Estimated Premiums

This example illustrates the use of the Estimated Percentage of Premium approach that may be elected by fully-insured plans. In the example, the Plan Sponsor is submitting two months of cost data. The insurer determines that the total Estimated Premium (EP) cost for the Plan Sponsor in January is $3,000.00 and in February is $3,000.00. Further, in determining the Estimated Cost Adjustment (ECA), the Plan Sponsor uses a methodology that allocates rebates as a percentage of incurred Part D drug costs for each Qualifying Covered Retiree between the Cost Threshold and Cost Limit. Under that methodology, the Plan Sponsor determines the ECA to be three percent.

In this example, $3,000.00 should be entered as the Estimated Premium (EP) for January and February. The ECA amount for January and February is $90.00 ($3,000.00 x 3%) each. The $90.00 is entered in the ECA column for both months; the Allowable Retiree Cost (ARC) for January and February is $2,910.00 ($3,000.00 - $90.00 = $2,910.00).

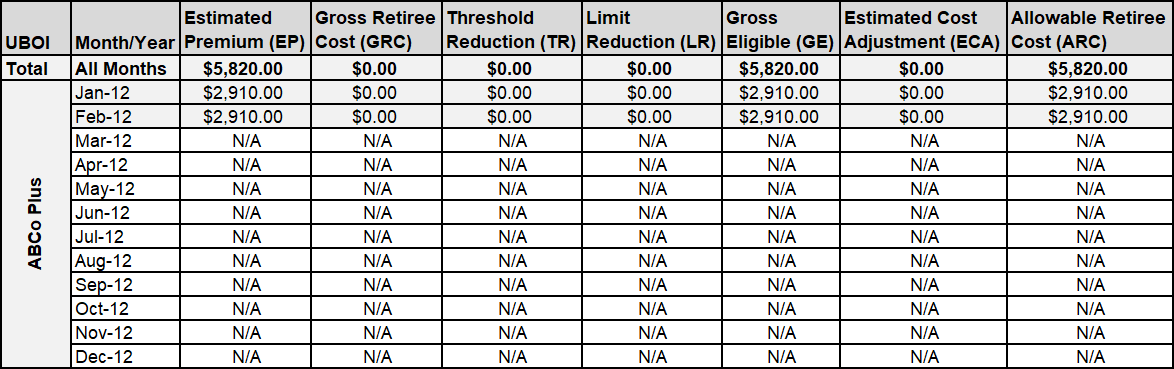

Estimated Premium (EP) With Estimated Cost Adjustment Taken Separately

If the Plan Sponsor prefers, the ECA can be accounted for by reducing the amount for the Estimated Premium. Accordingly, $2,910.00 would be entered as the Estimated Premium and $0.00 (or blank) would be entered as the Estimated Cost Adjustment. Either way, the Allowable Retiree Cost is $2,910.00.

Estimated Premium (EP) With Estimated Cost Adjustment Included

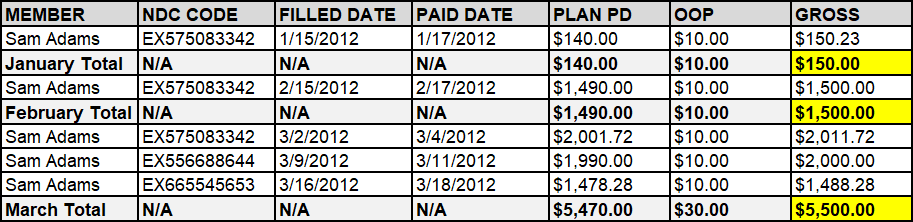

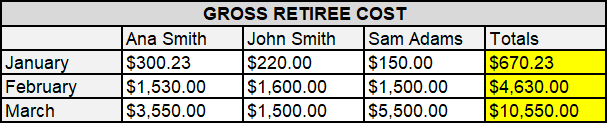

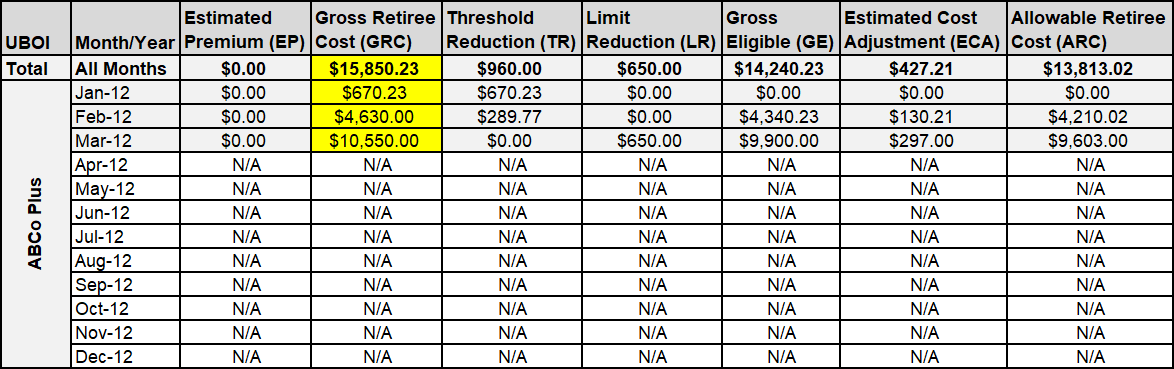

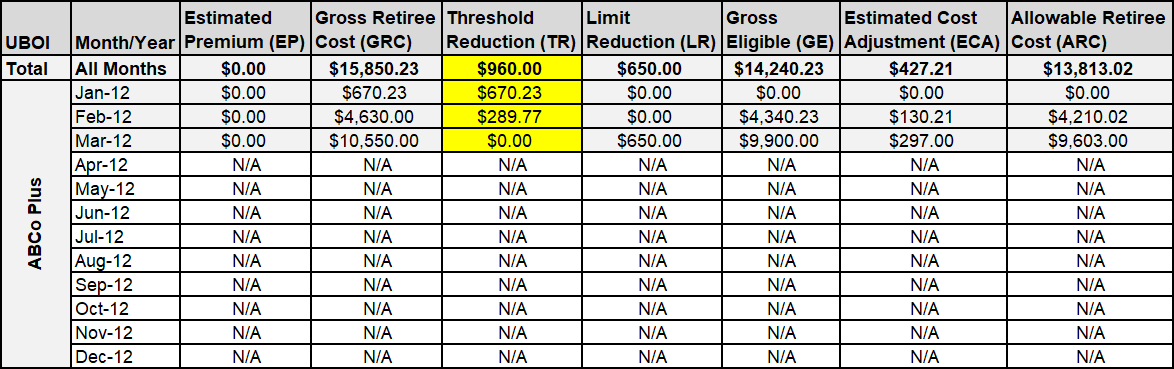

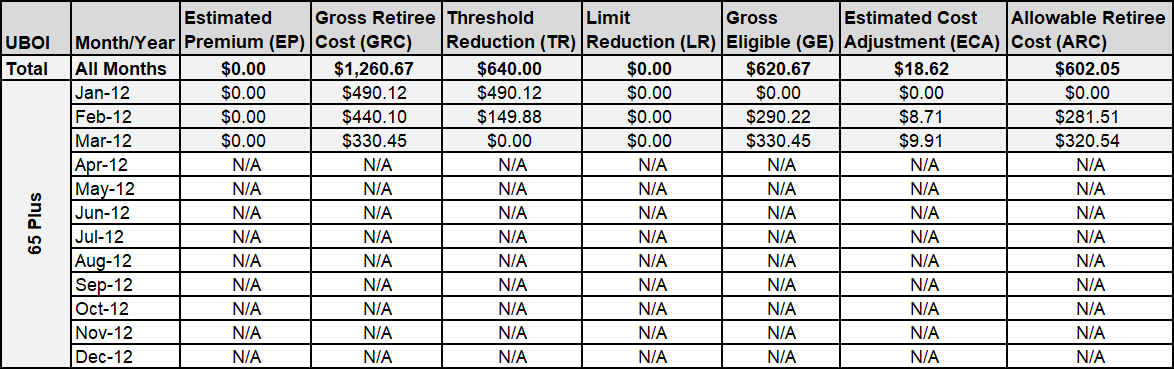

Cost Reporting Example Illustrating Gross Retiree Costs

This example illustrates cost reporting for plans reporting actual cost data, not estimated premiums. The Plan Sponsor for this example is a calendar year plan that has three retirees. As in the prior example, the Plan Sponsor uses a methodology that determines the Estimated Cost Adjustment to be three percent. The retirees have the following Gross Retiree Costs (GRC), the sum of the plan paid amount plus out of pocket expense:

Sample Retiree Data Gross Retiree Costs

-

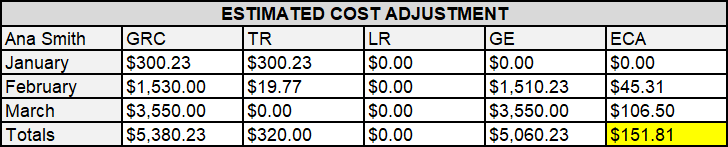

Ana Smith GRC: $300.23 ($280.23 + $20.00) for January, $1,530.00 ($1,510.00 + $20.00) for February, and $3,550.00 ($3,490.00 + $30.00) for March.

-

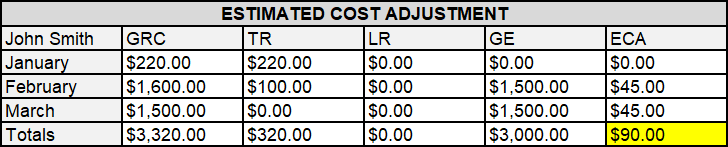

John Smith GRC: $220.00 ($210.00 + $10.00) for January, $1,600.00 ($1,590.00 + $10.00) for February, and $1,500.00 ($1,490.00 + $10.00) for March.

-

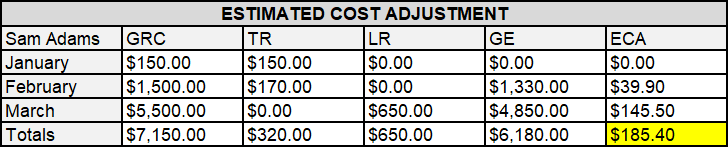

Sam Adams GRC: $150.00 ($140.00 + $10.00) for January, $1,500.00 ($1,490.00 + $10.00) for February, and $5,500.00 ($5,470.00 + $30.00) for March.

(Note: The examples are for illustrative purposes only. NDC codes reflected in these examples are not determinative of whether or not a drug is a Medicare Part D drug.)

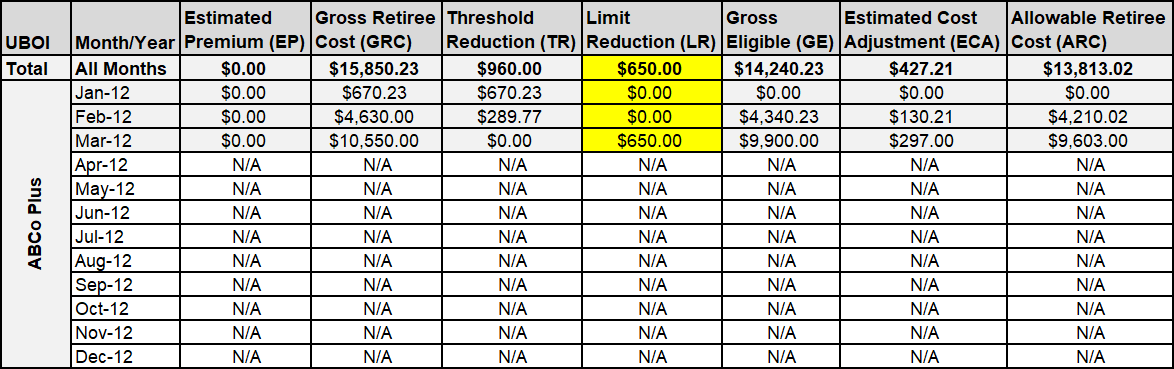

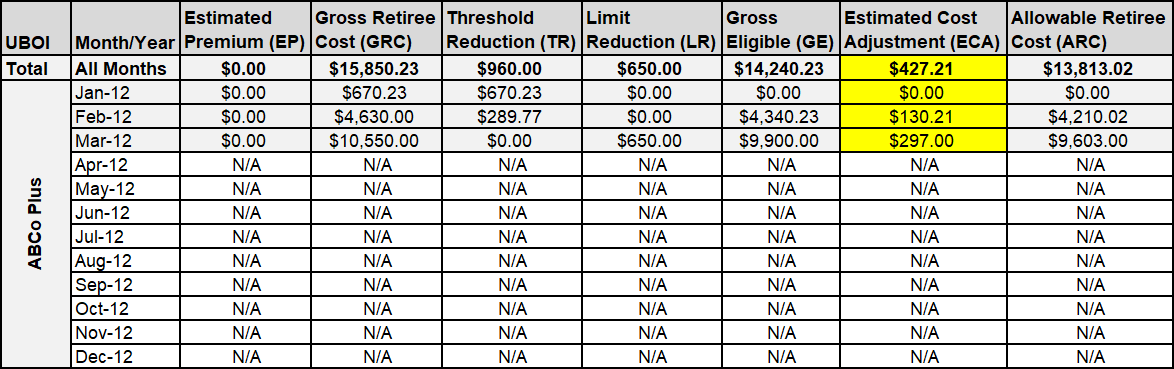

The total for January is the sum of the GRC for all retirees, or $670.33 ($300.23 + $220.00 + $150.00). The total for February is $4,630.00 ($1,530.00 + $1,600.00 + $1,500.00). The total for March is $10,550.00 ($3,550.00 + $1,500.00 + $5,500.00).

Sample Summary Data Gross Retiree Costs

In this example, the total Gross Retiree Cost is $15,850.23.

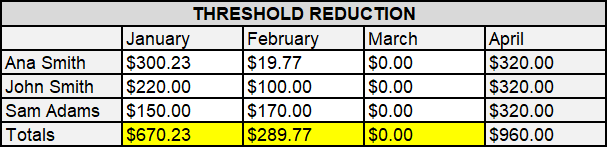

Cost Reporting Example Illustrating Threshold Reductions

In this example, the Threshold Reduction (TR) used is the $320.00 for plan years ending in 2012. For each retiree, the Threshold Reduction is calculated as follows:

Sample Retiree Data Threshold Reduction

- Ana Smith TR: $300.23 for January, $19.77 for February, and $0.00 for March.

- John Smith TR: $220.00 for January, $100.00 for February, and $0.00 for March.

-

Sam Adams TR: $150.00 for January, $170.00 for February, and $0.00 for March.

The total Threshold Reduction for January is the sum of the Threshold Reductions for all retirees, or $670.23 ($300.23 + $220.00 + $150.00).

The total for February is $289.77 ($19.77 + $100+ $170.00).

The total for March is $0.00.

Sample Summary Data Threshold Reduction

In this example, the total Threshold Reduction for January – March is $960.00.

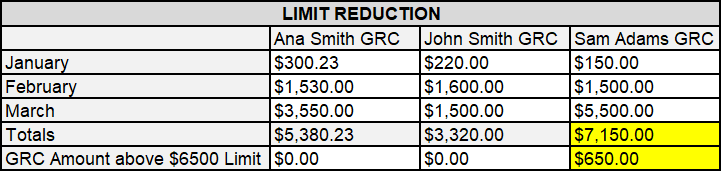

Cost Reporting Example Illustrating Limit Reductions

In this example, the Limit Reduction used is the $6,500.00 for plan years ending in 2012.

For each retiree, the Limit Reduction is as follows:

Sample Retiree Data Limit Reductions

- Ana Smith Limit Reduction: $0.00 for January, $0.00 for February, and $0.00 for March [total accumulated Gross Retiree Cost is less than $6,500.00).

- John Smith Limit Reduction: $0.00 for January, $0.00 for February, and $0.00 for March (total accumulated Gross Retiree Cost is less than $6,500.00).

-

Sam Adams Limit Reduction: $0.00 for January, $0.00 for February, and $650.00 for March [total accumulated Gross Retiree Cost is $150.00 + $1,500.00 + $5,500.00] – [the 2012 Cost Limit ($6,500.00)].

The total Limit Reduction for January is the sum of the Limit Reductions for all retirees, or $0.00. The total for February is $0.00. The total for March is $650.00 ($0.00 + $0.00 + $650.00). Sam Adams is the only retiree exceeding the $6,500.00 limit. In March, he exceeded the limit by $650.00.

Sample Summary Data Limit Reductions

In this example, the total Limit Reduction is $650.00.

Cost Reporting Example Illustrating Estimated Cost Adjustments

For each retiree, the Estimated Cost Adjustment (using the three percent of cost figure determined by the Plan Sponsor) is as follows:

Sample Retiree Data Estimated Cost Adjustment

-

Ana Smith Estimated Cost Adjustment:

For January, her gross eligible (GE) amount is $0.00 ($300.23 - $300.23 - $0.00); the ECA is $0.00. For February, her GE is $1,510.23 ($1,530.00 - $19.77 - $1,510.23); the ECA is $45.31 (GE x .03). For March, her GE is $3,550.00 ($3,550.00 - $0.00 - $3,550.00); the ECA is $106.50 (GE x .03).

-

John Smith Estimated Cost Adjustment:

For January, his GE is $0.00 ($220.00 - $220.00 - $0.00); the ECA is $0.00.

For February, his GE is $1,500.00 ($1,600.00 – $100.00 - $1,500.00); the ECA is $45.00 (GE x .03). For March, his GE is $1,500.00 ($1,500.00 - $0.00 - $0.00); the ECA is $45.00 (GE x .03).

-

Sam Adams Estimated Cost Adjustment:

For January his GE is $0.00 ($150.00 - $150.00 - $0.00); the ECA is $0.00.

For February, his GE is $1,330.00 ($1,500.00 - $170.00 - $0.00); the ECA is $39.90 (GE x .03).

For March, his GE is $4,850.00 ($5,500.00 - $0.00 - $650.00); the ECA is $145.50 (GE x .03).

Note: The ECA is applied to the Gross Retiree Costs between the Threshold Reduction and Limit Reduction (the gross eligible amount). Accordingly, if the gross eligible amount is $0.00 because the entire Gross Retiree Cost was applied to the Threshold or Limit Reductions, the ECA is also $0.00. The ECA will never be a negative number.

Sample Retiree Data Estimated Cost Adjustment

The total Estimated Cost Adjustment for January is $0.00 ($0.00 + $0.00 + $0.00).

The total Estimated Cost Adjustment for February is $130.21 ($45.31 + $45.00 + $39.90).

The total Estimated Cost Adjustment for March is $297.00 ($106.50 + $45.00 + $145.50).

Sample Summary Data Estimated Cost Adjustment

In this example, the total Estimated Cost Adjustment for January - March is $427.21.

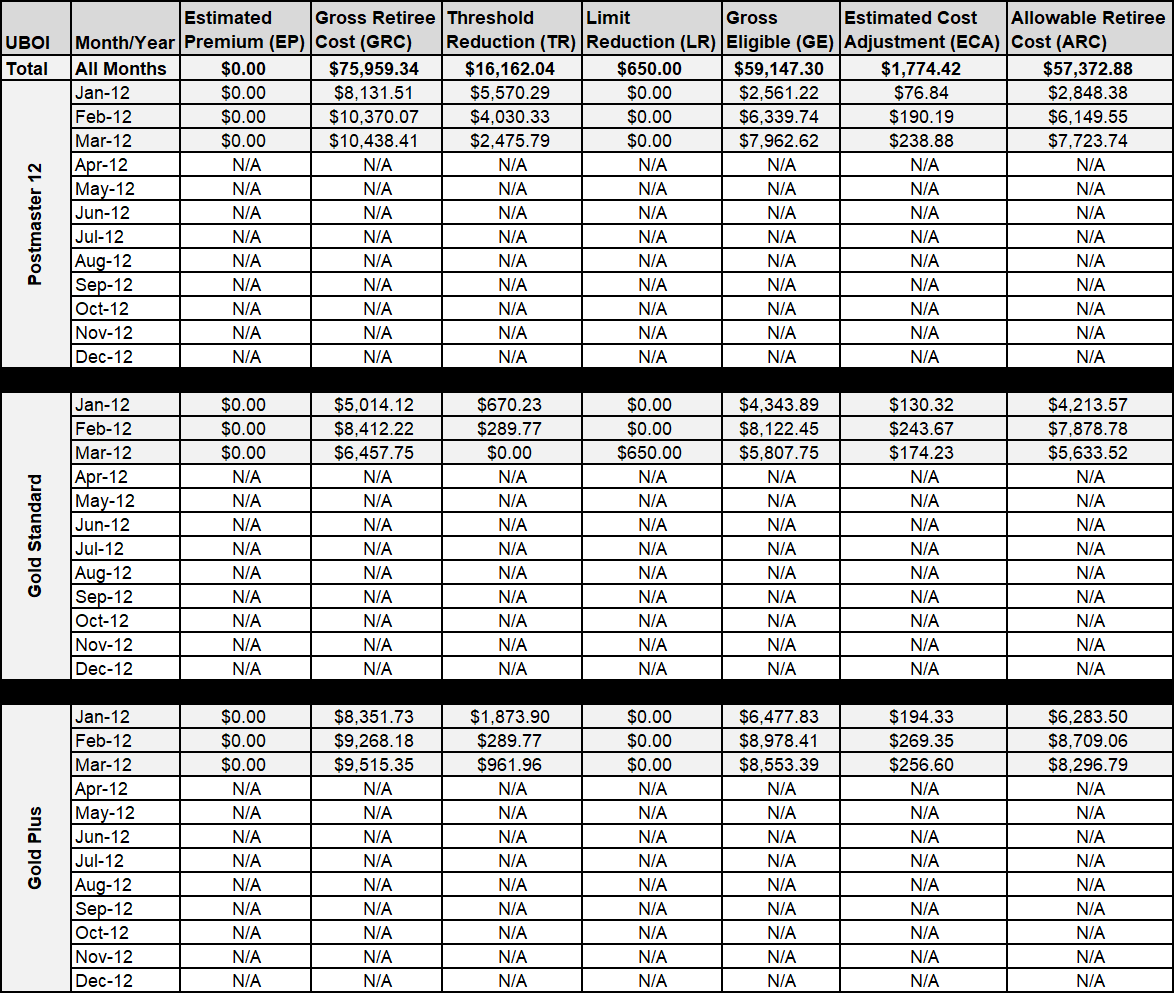

Cost Reporting Example Illustrating Multiple Benefit Options Reported Over Several Months

Sample Summary Data (Multi-Benefit Option)

In this example, the Plan Sponsor is reporting cost data for three Benefit Options. The Plan Sponsor is required to segregate cost data by Benefit Option and plan month. For each Benefit Option, cost data is being reported for three months (January – March).

Cost Reporting Example Illustrating Reporting Adjusted Costs

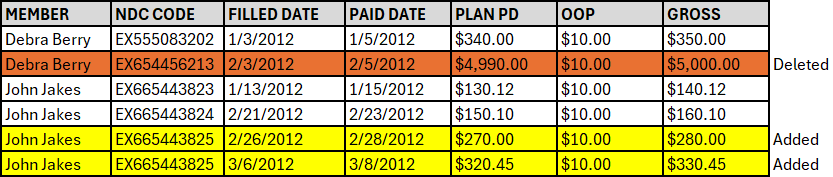

In this example, a Plan Sponsor has previously submitted cost data to CMS' RDS Center for an application with a plan year ending in 2012. The Plan Sponsor has to date reported cost data through February 2012 to CMS' RDS Center. When preparing to submit the cost data for March 2012, the Plan Sponsor sees that cost data for months previously submitted to CMS' RDS Center has changed, and new cost data was just received.

- Retiree 1, Debra Berry, incurred costs of $350.00 in January 2012, $5,000.00 in February 2012.

- Retiree 2, John Jakes, incurred costs of $140.12 in January 2012 and $160.10 in February 2012.

Each of the retirees above that incurred costs in 2012 incurred them while in retired (as opposed to active employee) status.

This information was reported to CMS' RDS Center in February 2012.

Sample Original Retiree Cost Data

(Note: The examples are for illustrative purposes only. NDC codes reflected in these examples are not determinative of whether a drug is a Medicare Part D drug.)

Sample Summary Cost Data

This example shows summary cost data for January and February.

However, when aggregating March 2012 cost data, new or revised cost data was realized for the previously reported months of January 2012 and February 2012 for the two retirees in this example.

Retiree 1, Debra Berry, incurred cost of $5,000.00 in January 2012 was deleted.

Retiree 2, John Jakes, incurred cost of $280.00 in February 2012 was just received.

Additionally, new costs for March of $340.45 need to be reported.

Revised Cost Data Received After Submitted to CMS' RDS Center

(Note: The examples are for illustrative purposes only. NDC codes reflected in these examples are not determinative of whether a drug is a Medicare Part D drug.)

Sample Summary Cost Data

This example shows revised summary cost data for January – March.

Note: Cost data for January was unchanged; therefore, it did not require a new submission. February cost had to be reaggregated and resubmitted because the original reported cost was changed. March cost data was being reported for the first time.

Cost Reporting Example Illustrating Gross Eligible Costs Exceeding Maximum Possible Gross Eligible

This example illustrates a cost reporting issue where the reported Gross Eligible costs exceed the total maximum Gross Eligible amount possible for the application based on the number of retirees contributing to the Threshold Reduction. If this issue is detected in Reconciliation: Review Final Costs, the RDS Secure Website displays an error message, and the Plan Sponsor is prevented from completing this step. Once the Plan Sponsor determines the error, it must Reopen Reconciliation: Manage Final Costs to once again allow reporting, update costs in Reconciliation: Manage Final Costs to resolve the issue, re-complete Reconciliation: Manage Final Costs, and proceed to Reconciliation: Review Final Costs.

Example

To calculate the maximum Gross Eligible for a given Benefit Option, CMS' RDS Center multiplies the plan year’s maximum Gross Eligible per individual by the Benefit Option’s maximum number of QCRs that can be contributing to the Gross Eligible amount.

In this example, assume a payment request for a 2011 plan year includes a Benefit Option that reports the following costs:

- Gross Retiree Cost (GRC) = $200,000

- Threshold Reduction (TR) = $5,000

- Limit Reduction (LR) = $20,000

The Gross Eligible (GE) amount is calculated by subtracting the reported Threshold and Limit Reductions (TR and LR) from the reported Gross Retiree Costs (GRC).

Calculation: $200,000 GRC – $5,000 TR – $20,000 LR = $175,000 GE

The maximum possible Gross Eligible is calculated by multiplying the plan year’s maximum Gross Eligible per individual by the maximum number of QCRs that can be contributing to Gross Eligible.

The plan year’s maximum possible Gross Eligible per individual is calculated as the plan year's Federally-defined Cost Limit minus the plan year's Federally-defined Cost Threshold. For the 2011 plan year the Cost Limit is $6,300, and the Cost Threshold is $310.

Calculation: $6,300 Cost Limit - $310 Cost Threshold = $5,990 Maximum Gross Eligible per Individual

In order for a Qualifying Covered Retiree’s Gross Retiree Costs to contribute to the Gross Eligible, Gross Retiree Costs for that individual must first surpass the Cost Threshold. The maximum number of individuals that can be contributing to Gross Eligible is calculated as the whole number resulting from dividing the reported Threshold Reduction by the plan year's Cost Threshold.

Calculation: $5,000 TR / $310 Cost Threshold as whole number = 16 Individuals (Maximum) Contributing to GE

The Maximum Gross Eligible calculation for this Benefit Option is as follows:

$5,990 Maximum Gross Eligible per Individual x 16 Individuals (Maximum) Contributing to GE = $95,840 Maximum Gross Eligible

In this example, the $175,000 Gross Eligible amount associated with the Benefit Option exceeds the $95,840 maximum possible Gross Eligible amount.